Technologies, finance, life, you name it

Market maps for today

Charts for today

11 Dividend stock picking criteria: is ENIA a good stock?

Value investor often look into those 11 creteria when evluating a dividend stock:

Criterion #1: Credit Rating Look for stocks with a grade of B+ or higher ( Moody’s www.moodys.com and Standard and Poor’s www.standardandpoors.com)

ENIA passed with its Baa3 rating. See the news below:

New York, December 19, 2019 — Moody’s Investors Service (“Moody’s“) today changed to positive from stable the outlook on Enel Américas S.A. (ENIA). Moody’s also affirmed the ‘Baa3‘ senior unsecured rating of ENIA.Dec 19, 2019

Criterion #2: Cash Flow Assessment

A strong cash flow allows a company to scale its operations and develop innovative products. It provides the means to fund dividend payouts . We look for Net Income growing at 5-10% per year (from Income Statement) – we also prefer stable or growing Operating Cash flow (From Cash Flow Statement).

We may use financial data from morningstar.

ENIA:

Net Income:

| 2017 | 2018 | 2019 | TTM | 3-Yr Trend |

|---|---|---|---|---|

| 0.71 | 1.20 | 1.61 | 1.61 | Increase every year |

Operating cash flow: ?

Not found in morning star for the last 3 years somehow.

Criterion #3: Cash & Cash Equivalents

We prefer a company with consistent growth in cash and cash equivalents, as seen from Balance Sheets from financial web sites such as morning star.

ENIA:

| 2017 | 2018 | 2019 | Q4 2019 |

|---|---|---|---|

| 1.58 | 2.05 | 2.04 | 2.04 |

Criterion #4: Debt Repayment Capacity

We prefer a company with a debt coverage ratio of at least 3:1.

We can use data from morning star.

debt coverage ratio = Net Income / (Interest Expenses + Other Payments)

Other payments could be principle, sinking, lease payments etc.

Interest Coverage is another ratio similar to debt coverage ratio above. The ratio is calculated by dividing a company’s earnings before interest and taxes (EBIT) by the company’s interest expenses for the same period.

Per WSJ, as of 09/11/2020, ENIA’s Interest Coverage is 3.29. PASSED.

https://www.wsj.com/market-data/quotes/ENIA/financials

Criterion #5: Management Performance

Read company reports as well as analyst reports. Understand its management team. Know the company’s long term growth and expansion plans.

ENIA: Recent quarterly call transcripts:

https://seekingalpha.com/symbol/ENIA/earnings/transcripts

Criterion #6: Current Dividend Yield

It should be at least 4% or 5%. ENIA: 12.51% (Paid Semiannually)

Criterion #7: Dividend Growth Rate

It should be at least 5%. Check out dividend.com and know the company’s dividend policy. ENIA: 5 years: 4.60%

Criterion #8: Dividend Payout Ratio

It should be less than 60% (check out dividend.com). Otherwise it cannot fund its growth.

Payout ratio of 60%-70% is acceptable only if its dividend yield is compelling (8-10%). Considering selling it if its payout ratio is too high.

ENIA Dividend Payout Ratio:

59.77%, PASSED (Based on Cash Flow, https://www.marketbeat.com/stocks/NYSE/ENIA/dividend/)

But other sites are showing different numbers:

122.43% (FWD PAYOUT RATIO, https://www.dividend.com/dividend-stocks/utilities/electric-utilities/enia-enersis-americashttps://www.marketbeat.com/stocks/NYSE/ENIA/dividend/-sa/#tm=3-ticker-best-div-capture&r=ES%3A%3ADividendStock%3A%3AStock%23ENIA–NYSE&f_28=true&only=meta%2Cdata%2Cthead)

114.03% – FAIL ??? (https://seekingalpha.com/symbol/ENIA/dividends/dividend-safety)

Criterion #9: ROE

ROE for the last 3 or more years is 12% or higher.

TTM ROE is at least 15%. Use financial data from morningstar/Key Ratios/Profitability.

During the past 13 years, Enel Americas/ENIA’s highest ROE % was 19.87%. The lowest was 7.46%. And the median was 11.22%. (https://www.gurufocus.com/term/ROE/NYSE:ENIA/ROE–ttm/Enel-Americas)

Enel Americas/ENIA’s return on equity, or ROE TTM, is 11.16% , as of 9/11/2020 (https://www.zacks.com/stock/chart/ENIA/fundamental/return-on-equity-ttm).

Criterion #10: Insider Activity

Buy when insiders are holding or buying more shares. Data can be extracted from:

a. Morningstar/Insiders/Insider Activity

b. Yahoo Finance/Insider Transactions

c. Zacks.com/More Research/Insiders

ENIA: No inside activities for the last 6 months: https://in.finance.yahoo.com/quote/ENIA/insider-transactions/

Criterion #11: Intrinsic value

Buy at or below its instrinsic value because your performance is determined not only by dividends but also capital appreciation.

ENIA: $10.66, current price $7.21 USD as of 09/11/2020. PASSED.

as of

| 12/31/2019 | 10.658 |

5G CIENA stock price: a similar ROE method to calculate its intrinsic value

Use a similar ROE model method described here:

Use the above mentioned calculator,

Cash Taken Out of Business ($): I entered 0 * This is dividends recieved for 1 year.

Current Book Value ($): 14.57 * We need to know this so we can determine the base value that’s changing.

Average Percent Change in Book Value Per Year (%): 6.67 * This will determine the estimate BV at the end of the next 10 years.

Years: 5 * This will most likely be 10 (if you’re comparing a 10 year federal note).

(Discount Rate) 10 Year Federal Note (%): 0.80 * Look up the ten year treasury note by clicking on this text.

Intrinsic Value ($): 19.33607699236469

I got this number as its intrinsic value:

19.33607699236469

The main difference is, I used 9% as discount rate when calculating NPV, while this calculator uses treasury 10-year note rate (0.80%).

Related blog posts:

ciena stock price: $44.28 is still overvalued based on my valuations

In my previous blog posts, I laid out a plan how to evaluate stocks using three methods.

In the blog post on how to evaluate a stock, I listed three methods when valuing a stock:

- P/E Multiple method

- DCF model

- Return on equity valuation method

I later dive deep into PE multiple method, and calculate CIEN’s intrinsic value as 39.7379.

If I believe my intrinsic value of CIEN, I will consider buying it below $39.73 per share. That’s close to its price 37.34 on Mar 27, 2020.

Before the broad stock market drop last week, CIEN was traded at 60.07 when market closed on Wednesday 9/2.

Yahoo Finance site says this stock price now is Near Fair Value.

According to GuruFocus, Ciena Intrinsic Value: Projected FCF : USD 33.40 (As of 9/5/2020).

Per https://trendshare.org/stocks/CIEN/view:

| CIEN Price (Ciena Corporation stock price per share) |

$59.93 | |

| [?] | CIEN Fair Price (based on intrinsic value) |

$25.84 |

| [?] | CIEN Safety Price (based on a variable margin of safety) | $15.50 |

In my latest blog post, I used ROE model and calculated the intrinsic value of CIEN as $23.74639 .

I later said,

The current share price $44.28 of CIEN as of Friday 9/5/2020 is very much overvalued, in my opinion.By the way, Ciena price target lowered to $37 from $53 at Barclays. Reiterate Underweight.Barclay’s analyst Tim Long lowered the firms price target on Ciena to $37 from $53 and keeps an Underweight weight rating on the shares. The company’s fiscal Q3 beat on sales, margin, and earnings; but guidance surprised to the downside.

So based on the above research, I think $23.74639 is CIEN’s intrinsic value, and the safe price to buy is around $15.50 for the margin of safety.

The current share price $44.28 of CIEN as of Friday 9/5/2020 is very much overvalued, in my opinion.

Disclaimer: I am just sharing my information, not suggesting you to buy any stocks or investments. Use the info here at your own risk. Please make your own judgements when making investment decisions.

How to evaluate a stock? The ROE valuation method, CIENA as example

Disclaimer: I am just sharing my information, not suggesting you to buy any stocks or investments. Use the info here at your own risk. Please make your own judgements when making investment decisions.

In my last blog post on how to evaluate a stock, I listed three methods when valuing a stock:

- P/E Multiple method

- DCF model

- Return on equity valuation method

Today I am going to deep dive into the third method: Return on equity valuation method.

We use Ciena (NYSE:CIEN) as an example. We’ll answer this question, is CIEN current price $44.28 over valued? Can I buy CIEN at this price?

Return on equity valuation method

Warren Buffet’s favorate metric of profitability is Return on equity (ROE).

In its simple terms, it is Net income / shareholder’s equity.

In general, 15% ROE or higher is good.

Let’s deep dive in, and see if CIEN is overvalued.

All new data inputs specific to this Return on equity (ROE) valuation method:

a. Return on equity, of the last 5 years

CIEN Return on Equity %:

| 2015-10 | 2016-10 | 2017-10 | 2018-10 | 2019-10 |

|---|

| 4.23 | 10.46 | 86.95 | -16.96 | 12.36 |

(Source: https://financials.morningstar.com/ratios/r.html?t=0P0000019J&culture=en&platform=sal)

(4.23+10.46 +86.95-16.96+12.36)/5=19.408

This results in Return on Equity % of 19.408% for the last 5 years.

b. Shareholders’ Equity

From Balance Sheet, the shareholders’ equity in the latest quarter (Q2 2020 at the time of this writing) is: 2.24 billion.

c. Dividend Rate

No devidend.

Dividend Payout Ratio: 0.00%

https://finance.yahoo.com/quote/CIEN/key-statistics?p=CIEN

Also accoding to Nasdaq, “Dividend History information is presently unavailable for this company.” (Source: https://www.nasdaq.com/market-activity/stocks/cien/dividend-history)

Other inputs:

a. Shares Outstanding 153.64M

b. Expected growth rate: Next 5 Years (per annum) 8.90%

This is the rate CIEN is expected to grow its profit in the next 5 years.

However, as we pointed out in a related blog post using PE Multiple Method, forecast is skeptical, especially Wall Street tends to provide higher estimate than in reality. So let’s apply some discount such as 25% as our margin of safety.

so 8.90%*(1-0.25)=0.06675

so let’s give it 6.67%, being conservative.

c. Discount rate: 9%, used to calculate NPV or intrinsic value.

Now let’s calculate is intrinsic value based on ROE model.

Shareholder equity per share: 2.24 billion/153.64 Million=$14.579536579

Let it grow at a conservative growth rate 6.67% (with margin of safety 25%).

In Year 1, CIEN has Shareholder equity per share $14.579536579.

In Year 10, it will be 14.579536579*(1+6.67%)^9=$26.0690002156.

Year 10 net income is the income per share which the shareholder equity in Year 10 can generate: 26.0690002156*19.408%=$5.05947156184

The required value is the amount of shareholders’ equity that is required if company just earns the average historical stock market return of 9%: 5.05947156184/9%=$56.2163506871.

This is the shareholders’ equity in Year 10. To calculate its worth today, we will apply discount rate 9% as NPV:

56.2163506871/((1+9%)^10)=$23.7463940545

If CIEN has dividends, we would have added to it the sum of the 10 years of discounted dividends.

This gives us an intrinsic value estimate for CIEN: $23.7463940545.

The current share price $44.28 of CIEN as of Friday 9/5/2020 is very much overvalued, in my opinion.

By the way, Ciena price target lowered to $37 from $53 at Barclays. Reiterate Underweight.

Barclay’s analyst Tim Long lowered the firms price target on Ciena to $37 from $53 and keeps an Underweight weight rating on the shares. The company’s fiscal Q3 beat on sales, margin, and earnings; but guidance surprised to the downside.

How to evaluate a stock? The PE multiple method, CIENA as example

Disclaimer: I am just sharing my information, not suggesting you to buy any stocks or investments. Use the info here at your own risk. Please make your own judgements when making investment decisions.

In my last blog post on how to evaluate a stock, I listed three methods when valuing a stock:

- P/E Multiple method

- DCF model

- Return on equity valuation method

Today I am going to deep dive into the first method: The PE multiple method.

We use Ciena (NYSE:CIEN) as an example. We’ll answer this question, is CIEN current price $44.28 over valued? Can I buy CIEN at this price?

P/E Multiple method

You determine stock’s five-year price target based on P/E valuation.

Those are all the inputs:

a. EPS (ttm): Earnings per share for the trailing twelve months is usually included in the stock information of a given stock in most financial websites such as morningstar.

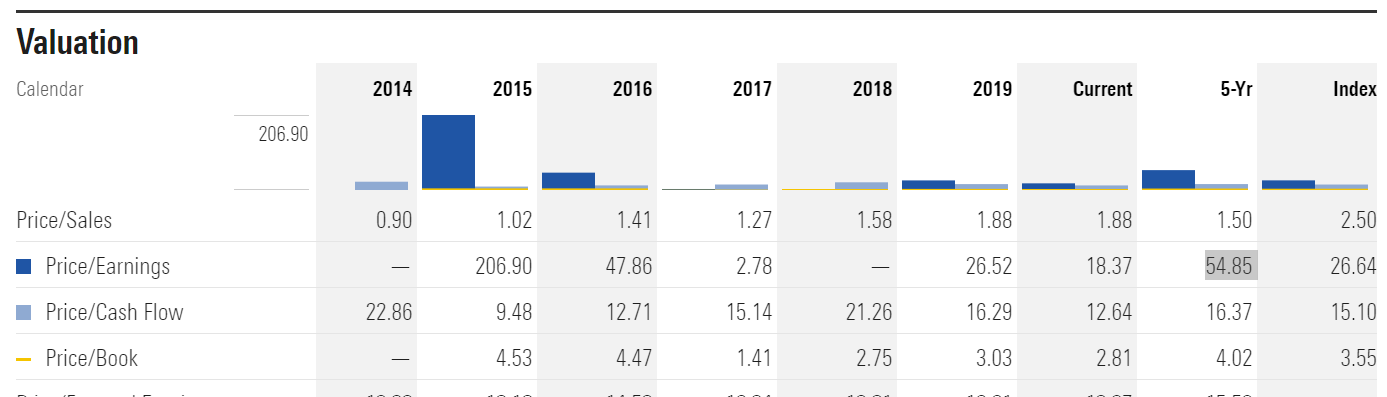

CIEN trailing twelve month P/E:

| EPS (TTM) | 2.41 |

Source: https://finance.yahoo.com/quote/CIEN?p=CIEN&.tsrc=fin-srch

b. the median historical price-earning multiple. We look at the past five years.

| 54.85 |

Source: https://www.morningstar.com/stocks/xnys/cien/valuation

Per YChats, it is 54.37 (Average, Past 5 Years; https://ycharts.com/companies/CIEN/pe_ratio)

It’s PE as of Friday Sept. 4, 2020 is 18.37.

c. Expected growth rate

Next 5 Years (per annum) 8.90%

Source: https://finance.yahoo.com/quote/CIEN/analysis?p=CIEN

This is the rate CIEN is expected to grow its profit in the next 5 years.

However, forecast is skeptical, especially Wall Street tends to provide higher estimate than in reality. So let’s apply some discount such as 25% as our margin of safety.

so 8.90%*(1-0.25)=0.06675

so let’s give it 6.67%, being conservative.

Next, we put all those together to get the price target for the next 5 years:

EPS*avg hist P/E ratio*growth rate^5, that is:

2.41*54.85*(1+6.67%)^5=182.559799432

This is the price target in 5 years for this stock.

However, we are most interested in the intrinsic value of this stock now so assuming stock market returns 9% annually, here we calculate the intrinsic value of the stock (or we call it Net Present Value, NPV):

5-year price target / (1+9%)^5, that is:

182.559799432/(1+9%)^5=118.651343527

You can replace it with other numbers instead of 9% if you want to achieve say 20% per year for the next 5 years.

As you can see, if you feel avg hist P/E ratio (for the last 5 years) 54.85 is comfortable, CIEN is a great bargain, as at the time of this writing as it is trading at 44.28 at the close of 9/4 Friday, after two consecutive drops of the broad stock market last week.

Somehow I don’t feel this PE for the last 5 years for CIEN is good to estimate for the next 5 years, as its value was spiked because of some sudden PE changes in 2015 such as this peak PE:

| Maximum | 281.11 | Nov 27 2015 |

So if I use current PE 18.37 (as of 9/4/2020 Friday market close) I have the following target price for this stock:

2.41*18.37*(1+6.67%)^5=61.1417231643

NPV for current:

61.1417231643/(1+9%)^5=39.7379248968

If I believe my intrinsic value of CIEN, I will consider buying it below $39.73 per share. That’s close to its price 39.34 on Mar 27, 2020

Before the broad stock market drop last week, CIEN was traded at 60.07 when market closed on Wednesday 9/2.

Yahoo site says this stock price now is Near Fair Value.

According to GuruFocus, Ciena Intrinsic Value: Projected FCF : USD 33.40 (As of Today).

https://trendshare.org/stocks/CIEN/view:

| CIEN Price (Ciena Corporation stock price per share) |

$59.93 | |

| [?] | CIEN Fair Price (based on intrinsic value) |

$25.84 |

| [?] | CIEN Safety Price (based on a variable margin of safety) | $15.50 |

How to evaluate a stock?

When you walk in super markets, you’ll see the retail values keep changing on different days across different stores. But you kind of know the value of those things you buy every day, though their prices fluctuate depends on time and location. In other words, you know the intrinsic values of those things in super markets.

The same goes with stock market, with a market of stocks. How do you know the intrinsic values of each stock?

- P/E Multiple method

- DCF model

- Return on equity valuation method

Let’s briefly talk abour each of those evaluation methods. I will provide more details in future blog posts so stay tuned.

- P/E Multiple method

You determine stock’s five-year price target based on P/E valuation.

a. EPS (ttm): Earnings per share for the trailing twelve months is usually included in the stock information of a given stock in most financial websites such as morningstar.

b. the median historical price-earning multiple. We look at the past five years.

c. Expected growth rate

This is the rate a stock is expected to grow its profit in the next 5 years.

Next, we put all those together to get the price target for the next 5 years:

EPS*avg hist P/E ratio*growth rate

This is the price target in 5 years for this stock.

However, we are most interested in the intrinsic value of this stock so assuming stock market returns 9% annually, here we calculate the intrinsic value of the stock (or we call it Net Present Value, NPV):

5-year price target / (1+9%)^5

You can replace it with other numbers instead of 9% if you want to achieve say 20% per year for the next 5 years.

2. DCF model

We take the trailing twelve months FCF, project it 1o years into the future by multiplying it with an expected growth rate. It then takes the NPV of these cash flows and adds them up.

We assume the company will be sold after 10 years from now. – so we have the Year 10 FCF * factor (12, a number b/w 10-15)

a. Free cash flow, FCF: the trailing twelve month FCF, shown in Cash Flow statement.

b. Cash and cash equivalents: shown in the company’s latest quarterly Balance Sheet report.

c. Total liabilities: all debts

d. Growth rates: as we used in Method 1, but we may apply 25% discount for the margin of safety.

Just as in Method 1, we may use 9% as our discount rate.

e. Shares outstanding: We need to know the intrinsic values per share.

The total NPV PCF is the sum of all the cash flows.

Year 10 FCF value: Year 10 FCF multiplier (12) * NPV of FCF in Year 10

3. Return on equity (ROE) valuation method

Warren Buffet’s favorate metric of profitability ROE.

Net income / shareholder’s equity.

15% ROE or higher is good.

All inputs:

a. Return on equity

b. Shareholders’ Equity

c. Dividend Rate

It’s freaking difficult to migrate WP blogs

You would think it is easy, export, import, then bang, all works!

Not that easy.

Unless it’s a toy web site with a few pages, your import process will time out. The share host environment for example will terminate your import process in a few mins.

I looked online. I may try “WordPress WXR File Splitter (RSS XML) — Updated v1.52!”

I have to split my WXR file into smaller chunks, then import a few times.

Shame on WordPress, for a software being there for years, still the import/export features will not actually work for most users.